[$TTCF] Tattooed Chef Stock Analysis & Insights

[$TTCF] Tattooed Chef Stock Analysis & Insights

Deep Dive into Tattooed Chef $TTCF the plant based foods company.

———Insightful Diligence [Deep Dive]———

Problems

The demands of consumers seek to follow a natural and “cleaner-label” diet. But there is a lack of products sustainable, ethically sourced, wholesome and delicious, readily available, high-quality, clean-label, ready-to-cook, and plant-based. Therefore it’s hard to find many uncompromising companies products that offer all of this. Check out the following graphics of which I got from this amazing read

Why do they do it (Mission)?

Tattooed Chef’s mission is to deliver high quality and great tasting plant-based foods to consumers who care about sustainable and ethically sourced foods. The brand’s tagline, “Serving Plant-Based Foods to People Who Give a Crop”, aims to convey the brand’s mission.

*This brand’s tagline and culture if you can’t tell already is very catchy, unique, and one of which I personally love and that’s why you can understand that this company has such a strong community obsessed with it which leads to strong sales & a rapidly growing online footprint represented by many things but one is 250%+ Email List Growth.

What does the company do (Solutions)?

Tattooed Chef, Inc. $TTCF is the mission driven company we are talking about today and is headquartered in Paramount, California and serves plant based foods to people who give a crop! With 62+ expected SKUS in 2021 and 100+ products in development they have much to offer for consumers & for potential investors. They are in 6065 stores with 31K points of distribution & the company expects 7,227 stores and 39K points of distribution by the end of Q2 ending in June. Their 2021 objective is 10K stores & 65K points of distribution.

$TTCF creates and develops new products to address emerging market demands and food trends for healthy, plant-based foods. Here are a couple examples below.

*They saw a need for better and tastier plant based options, utilizing sustainably sourced ingredients. Eating food is personal and often looks different from one household to the next. Therefore Tattooed Chef offers a wide range of plant based foods to fit into many different lives, routines, and diets. Their innovative plant-based products offer consumers a diverse portfolio of wholesome, clean label items that are convenient, without sacrificing on quality, nutritional value or freshness and that are great tasting.

“We believe that our high-quality, clean-label, ready-to-cook, plant-based products fill a void in the marketplace and are well received by our target customers.” - Tattooed Chef’s 10K

Tattooed Chef as a company has established branded & private label products of which they serve to customers.

*Revenues from Tattooed Chef branded products grew from approximately 22% of their total revenue in Fiscal 2019 ($18.3 million) to approximately 57% of their total revenue in Fiscal 2020 ($84.6 million). As of Q1 2021 the branded products is now about 69% of total revenues

Tattooed Chef products are primarily sold in the frozen food section of retail stores and club stores and are available in all 50 states. Tattooed Chef also has an ecommerce platform which will help in revenue growth and delivering on their mission.

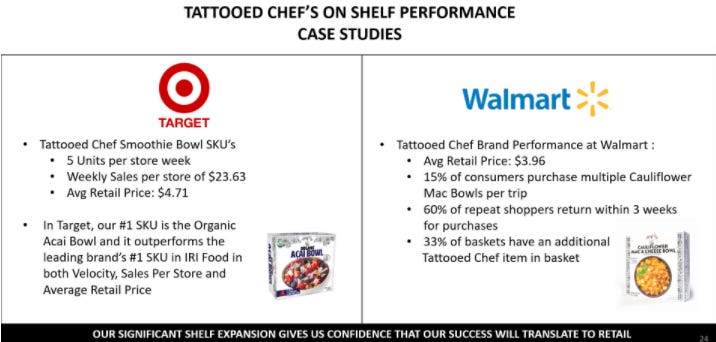

As far as the validity of demand of their products there is many ways to tell customers like it but for one Target said their launch of the entree bowl line was the most successful frozen food launch in the HISTORY of Target!

How do they do it (Solutions Explained)?

Tattooed Chef is a vertically integrated company. They source most of their ingredients in Italy, where they contract the fields and plant their own crops, but primarily manufacture in USA and are not dependent on any single grower in Italy for any single commodity. As well as source strawberries and other certain crops in the USA. They source their vegetables from a number of growing regions within Italy, and North and South America.

As I previously stated Tattooed Chef has established branded & private label products of which they distribute to customers. They also have been growing the branded products as a % of revenues which should help reduce customer concentration and further grow their brand. They believe the branded products could grow to 75%-80%+ of their revenues in the upcoming years.

*Also note they have not issued any patents and are not pursuing too as they consider these things as trade secrets and the information confidential.

They believe the growth of their Tattooed Chef branded products will be a key driver of revenue growth through new product launches and additional customers. They also believe that as this product line grows, they should be able to achieve economies of scale and continuing margin improvement. To the point of conservative expectations in 2026 of Adjusted EBITDA being 20%+ as a % of sales, Gross Margin 35%+ as a % of sales, and revenues of $1 Billion, (the management’s 2021 guidance does not include acquisitions). Which they just made an acquisition which they think can pull in 200M in revenue annually 2-3 years down the line. This sales CAGR not including acquisitions to 1 billion would represent about a 35% CAGR! Also their rapid growth thus far from 2020 and back is all organic growth.

*See page 34 of the December 2020 investor presentation below👇🏾

Although Tattooed Chef recently entered in agreement to acquire New Mexico Food Distributors & Karsten Tortilla Factory and cost them $35 Million in cash which adds two new facilities (totaling 118K square feet) to their previous two facilities expanding production capacity and allowing them to diversify manufacturing capabilities as well as grow their product portfolio even faster. This all gives them a total of over 275K square feet.

In two to three years we believe Foods of New Mexico can contribute up to $200 million in revenue annually. The focus going forward will continue to be on Tattooed Chef branded plant-based products. - Q1 2021 Earnings Call Sam Galletti

And by the end of Q2 tattooed chef products will be available at Whole Foods adding already to their huge footprint of stores that their products are located in such as Costco, Target, Walmart, Kroger, etc. Which btw those companies account for a lot of grocery spend in the US. In addition to all of this in Q3 they already have commitments from albertsons & sprouts.

They also utilize food brokers to assist in establishing and maintaining relationships with certain key customers, which represent the bulk of their revenue. They have written agreements with several different brokers, each of whom facilitates their relationship with a different key customer. Pursuant to these agreements, their brokers are entitled to a commission based on the revenue they facilitate between them and our key customers. So aligned interest.

*Commissions range from 1.5% to 3.0% of sales, with the exception of one broker to whom they owe commissions equal to 5.0% until sales through that broker exceed a certain threshold. The loss of any one of these food brokers could negatively impact the customer relationship resulting in their business, results of operation and financial condition being adversely affected.

Also tattooed chef sells outcomes along with products to retailers as you can see

Competition

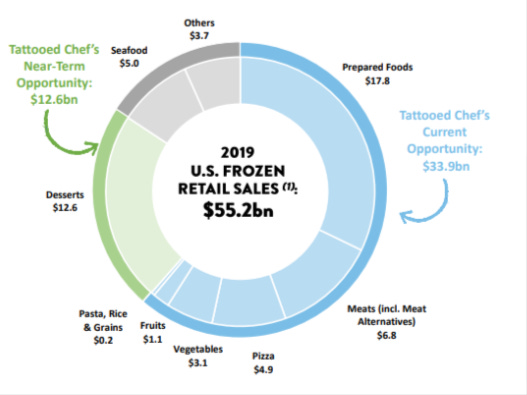

They compete with companies that produce products in the plant-based, vegetarian, and frozen food categories, such as Sweet Earth (Nestle), Birds Eye (Conagra Brands), Amy’s, and Green Giant (B&G Foods). Additionally, a number of United States and international companies are working on developing or promoting plant-based products. They compete with companies that operate in the highly competitive plant-based and frozen food segments, many of which have greater financial resources, better connections, and a stronger footprint. The principal competitive factors in this category include, among others, taste, nutritional profile, ingredients, cost and convenience. They participate in the $55 billion North American frozen food category.

This obviously means that they have a lot of competition because they had only 148.5M in revenue for 2020 and sit at about a 1.8 Billion Market Cap in 2021. But as far as competitors go anyone can create a healthy product it just depends on which has the best taste that is most broadly liked, distributed the most, and also at the best price or value. These decisions ultimately come down to the innovators in these companies and the consumers decisions on if they like it for the price they pay and needs they must have.

Seasonality

Historically they’ve experienced moderate revenue seasonality, with the third and fourth fiscal quarters generating higher sale amounts due to product demonstration schedules, new SKU promotions, increased demand in the summer season, and retailers allotting additional freezer space for holiday items. They expect that seasonality in revenue will decrease as their business grows and additional products are introduced. Also as far as covid-19 impacts the management speaks on this toward the end of the analyst day dec 2020 call and basically saying looking forward they dont expect pretty much any impact of covid on sales also in the past effects of covid were minimal because of the fact of which they operate in they said it basically insulated them.

Management

“I prefer to sail in a bad ship with a good captain rather than sail in a good ship with a bad captain.” - Mehmet Murat ildan

So obviously a ship is of no use without a good captain and at the end of the day the team you build is the company you build. So analyzing management is important and one of the determining factors if I buy a company or not so we will deter from the previous a little bit to stop and analyze management. Their executive management team, is led by Salvatore “Sam” Galletti, their innovation efforts are led by Sarah Galletti, and includes individuals who possess substantial industry experience. Cumulatively, their management team has over 160 years of industry experience, with an average of 25 years’ experience in the food industry, and an average tenure with them of seven years. Sarah Galletti the Creative Director is of course related to Sam Galletti the CEO. Sarah is the brains. The Tattooed Chef brand was created in 2017 and is the brainchild of Sarah Galletti, their Creative Director, based on her experiences with various food cultures while travelling internationally. She recognized a lack of readily available, high-quality, clean-label, ready-to-cook, plant-based products, which formed the foundation of Tattooed Chef. The insiders collectively owns more than 40%+ of the company. Also for more information on the amazing leadership at the company just research it yourself using various reputable sources such as linkedin and the investor relations page etc.

Financials & Growth

Market Cap of $1.8 Billion

Enterprise Value of $1.64 Billion

Revenue increased by $63.6 million, or 74.9%, to $148.5 million for Fiscal 2020 as compared to $84.9 million for Fiscal 2019 and also increased from revenues of $47.3 million in 2018.

The revenue increase was due to an increase of $66.3 million in volume for Tattooed Chef branded products, primarily driven by expansion in the number of United States distribution points, increased revenue at existing club channel customers and new product introductions. - Tattooed Chef 10K

The increase in branded product sales was partially offset by a $0.9 million decline in private label products and a $1.8 million decline in legacy products that are expected to be phased out in future periods. We anticipate continued growth in Tattooed Chef branded products primarily due to new product introductions, further expansion with current customers and increased sales to new retail customers. While we are primarily focused on growing our branded business, we will continue to support our current private label business and will evaluate new opportunities with these customers as they come. - Tattooed Chef 10K

Also in their 10K between F-19 to F-20 it shows this

Also an interesting thing I heard in the december 2020 analyst day conference call for tattooed chef is an interesting statistic is that 20% of the skus of a brand represent about 80% of their revenue. This is an opportunity for them because they produce skus that sale really well (represented by the case studies) and that are highly differentiated so if they can replace those skus that don’t sale the company such as say a walmart can generate more revenue and so can tattooed chef. In the call they further state that this is a selling point they use along with them being vertically integrated etc. which further speaks to the managements genius & competence.

Also Q1 2021 revenue alone was 52.7M. And the company anticipates $235M-$242M in revenues for year end 2021. We know this is conservative for many reasons but one obvious one is because this guidance doesn’t include any revenue contribution from the 2nd facility they call Karsten as its not in operation although they believe production begins in that facility in the coming months.

Gross profit increased $10.0 million, or 72.5%, to $23.7 million for Fiscal 2020 as compared to $13.7 million for Fiscal 2019. Gross margin for Fiscal 2020 was 15.9% as compared to 16.1% for Fiscal 2019.

The slight decrease in gross margin was due to increased cost of raw materials and other manufacturing expenses offset by production efficiencies associated with larger sales volume in Fiscal 2020 compared to Fiscal 2019.

The Company anticipates $235M-$242M in revenues for year end 2021 and increases in gross profit in 2021 and beyond due to higher sales volume. They also anticipate higher gross margins in 2021 and beyond due to operating efficiencies and leverage of fixed manufacturing costs. Also they expect at least 300M in revenue in 2022.

The lower costs in the future will come from operating efficiencies such as per person managing more amount of lbs of produce or product etc. as they scale which should obviously drive gross margins up.

Adjusted EBITDA increased by $2.7 million to $9.6 million for Fiscal 2020 as compared to $6.9 million for Fiscal 2019. The improvement in Adjusted EBITDA was primarily the result of the increase in revenue and gross profit, partially offset by increased operating expenses to support the growth in revenue, brand recognition for Tattooed Chef, and, beginning in the fourth quarter of Fiscal 2020, increased general and administrative costs resulting from being a public company as compared to the prior-year period.

In 2020 dont let that net income throw off your projections as they had a huge one time income tax benefit of $40,278,000.

“Excluding the non-recurring gain on derivative related to the settlement of contingently redeemable equity, the one-time tax benefit resulting from the change in tax status, and the one-time compensation expense described in “—Operating Expenses”, net income for Fiscal 2020 would have been $5.4 million, or $0.2 million less than Fiscal 2019, as increases in gross profit were offset by increased investment in the Tattooed Chef brand and costs incurred to transition to a public company, including stock-based compensation expense.”- Tattooed Chef 10K

I am not worried about profitability rn bc they’ve had a history of showing they can be profitable and in their recent quarter Q1 2021 they weren’t profitable but it isn’t a big deal as they are in a growth stage and showed they can pull profitability off.

Approaching $200 million of cash.

About 287.4 million of stockholders equity

Shares Outstanding of 81.94m

Objections (Reason for Undervaluation)

Pitti the Pessimist: During Fiscal 2020, Tattooed Chef sold a substantial portion of their products to three customers, which accounted for approximately 88% of Fiscal 2020 revenue. These three customers individually accounted for approximately 39%, 32%, and 17% of their Fiscal 2020 total revenue, respectively. In addition, three customers accounted for approximately 87% of their accounts receivable as of December 31, 2020. These three customers individually accounted for approximately 53%, 24%, and 10% of their 2020 total accounts receivables. This seems scary as if anything goes wrong which anything can go wrong no matter how strong of a relationship someone thinks they have, Tattooed Chef would see massive revenue decline and the management’s guidance in the future could be really wrong as one of their customers could essentially wipe out a lot of revenue.

Mya the Optimist: Everything you said is true and the company seems to try and hide this fact by comparing 3 customers collective % of revenues to 5 customers collective % of revenues over a year timespan. When it would obviously be better to compare 5 customers to 5 customers or 3 customers to 3 customers. And you can understand this is a risk by further going down the 10K between F-12 and F-13.

Although this is a risk the company is overcoming these risks. In their 10K they stated the following

“As we grow “Tattooed Chef,” we expect to expand our sales and marketing team by adding more dedicated personnel to service additional retail customers. We are also contemplating adding outside sales representatives and/or brokers to extend our sales efforts. These efforts to add retail customers could partially mitigate customer concentration risk.” - Tattooed Chef’s 10K

Pitti the Pessimist: What about that short interest though? This company could get shorted down

Mya the Optimist: With recent short squeezes such as with gamestop and amc etc. i doubt that and the fact that this company is growing quickly fundamentally i doubt that. Personally i dont count short squeezes as a huge risk to invest in a fundamentally strong company for a company of 1B+ market cap. I might be dumb for saying that but its like what do i believe that others don’t believe.

Pitti the Pessimist: What about those prices for the products it seems pretty expensive for the product?

Mya the Optimist: Yah my mom said that too but the thing is that to be brutally honest they do seem to be a little expensive. But you know what it’s obviously at a good enough price that people are repeatedly buying it and has driven sales massively (all organic growth) where it beats management’s expectations & the consensus expectations consistently.

Pitti the Pessimist: Fair point, but then what about the stock price, it’s a little different there because price does matter a lot more and every great company isn’t a great investment. You personally havent touched on anything but the fundamentals not really the bull case.

Mya the Optimist: I agree here’s my insights (3 min read) https://momentousinsights.substack.com/p/ttcf-tattooed-chef-stock-quick-pitch

Are you interested in the stock market but need questions answered?

Fill out this form ⬇⬇⬇ and I will try and help you (for FREE)

https://forms.gle/G4Eq1a4QR66X7rmT6

All you have to do is ask the question!

——————————Closing——————————

{Thankyou for reading. Hopefully you found this as insightful, if you did you can follow me on various socials linked below for more}

Socials & Other Substacks

YOUTUBE: SUBSCRIBE HERE

TWITTER: FOLLOW ME HERE

DISCORD: JOIN US HERE

SUBSTACK: SUBSCRIBE HERE

Disclaimer & What I’m Invested Into

Perfection is just a direction - Elayne Quirin

Do remember perfection is just a direction and i don't buy or sell stocks bc of relative or absolute valuations.. I use this as guidance nothing more nothing less.

As of June 14th, 2021 at 1:30 PM CDT im invested in $DBX $TTCF $IDKFF $PKKFF $FUV